As Bitcoin (BTC) stagnates between the $29K and $30K levels, sentiment about the leading cryptocurrency has nosedived to levels last seen during the onset of the Covid-19 pandemic in March 2020.

Market insight provider Santiment acknowledged:

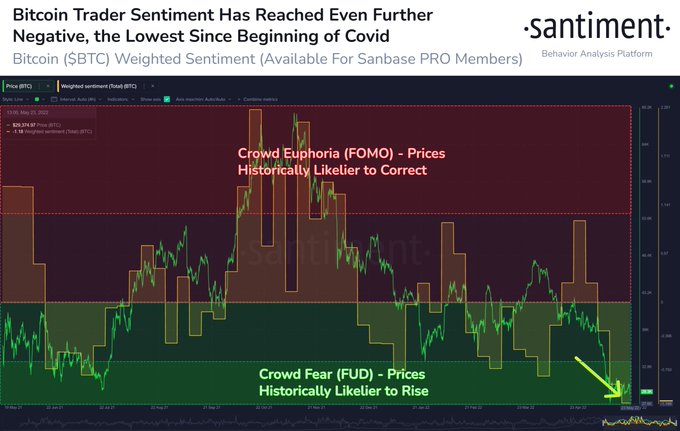

“Bitcoin’s sentiment is at rock bottom, indicating the amount of doom and gloom surrounding BTC and crypto in general is at its most negative since BlackThursday in March, 2020. Weak hands may continue to present opportunities for the patient.”

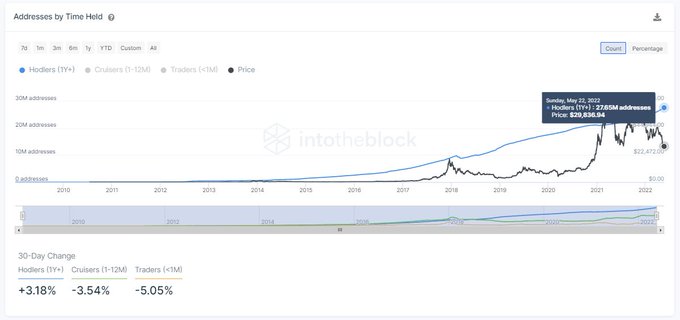

Source: SantimentNevertheless, this seems not to be dampening the spirits of BTC hodlers, who have accumulated for more than a year based on linear growth. Data analytic firm IntoTheBlock pointed out:

“Regardless of the recent price action, BTC hodlers have remained unfazed, as the linear growth continues. The number of holders (address holding >1year), is currently at an all-time high. There are now 27.65m addresses holding 12.66m BTC for more than 1 year.”

Source: IntoTheBlockBitcoin has been in the red for eight consecutive weeks. This bearish run has been fueled by Fed’s interest rate hike and the recent Terra crash.

As a result, the top cryptocurrency has been trading in the extreme fear zone based on the hiccups witnessed in the market.

On the other hand, various analysts have hinted that Bitcoin might be edging closer to bottoming out.

For instance, PlanB, the creator of the Stock-2-Flow (S2F) model, recently noted that the relative strength index (RSI) and realized price/moving average (RPMA) indicators had hit rock bottom, showing that the present bear market was almost over.

Moreover, market analyst Ali Martinez stated that BTC funding rates continued to be negative because short positions were dominant. Therefore, this was a positive sign for a rebound in BTC price.

Bitcoin was hovering around $29,188 during intraday trading, and it needs to hold the significant support level of $29K to increase its chances of a reversal.

Image source: Shutterstock

Credit: Source link

{kind=link}